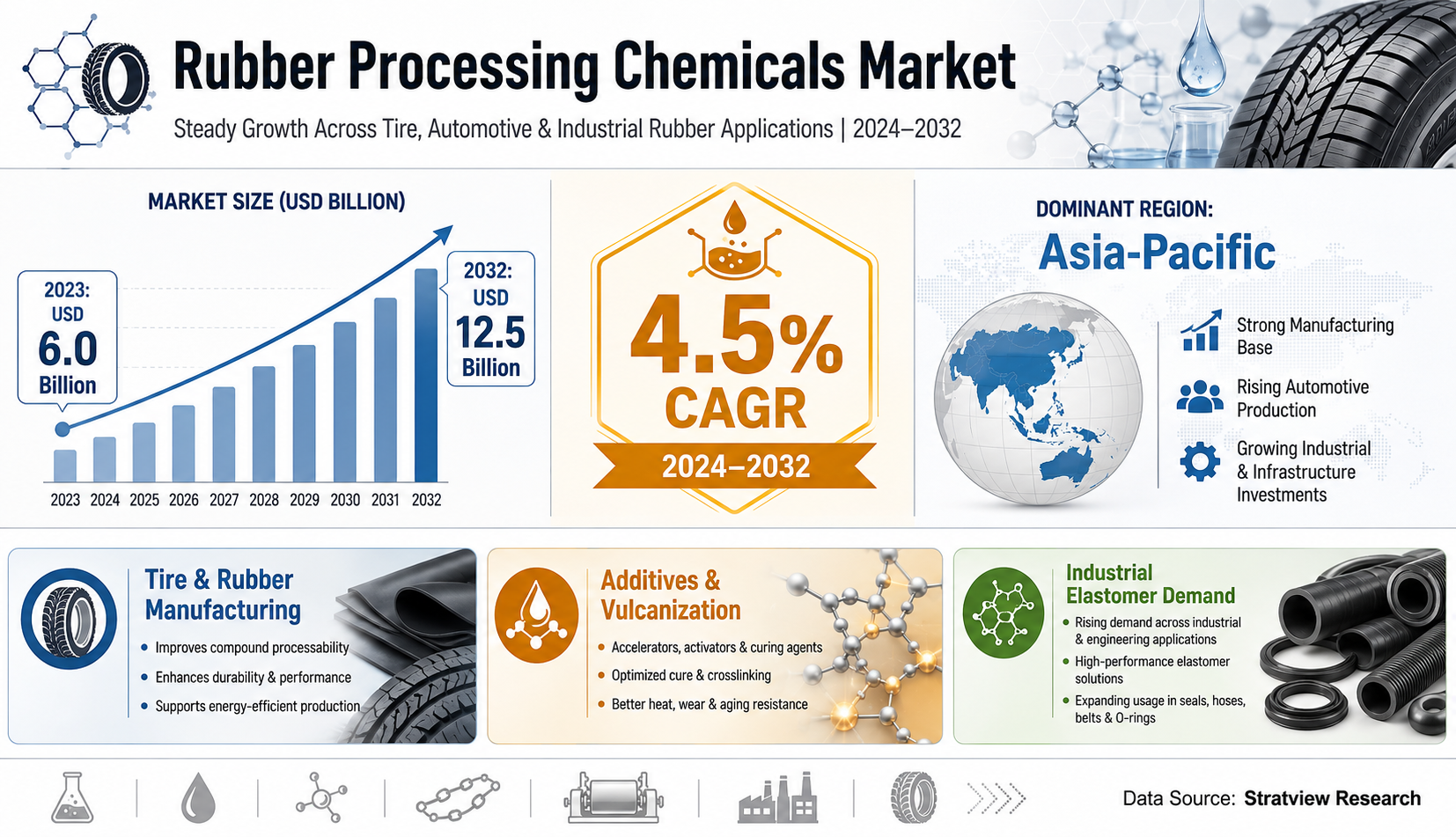

The Rubber Processing Chemicals Market stood at USD 6.0 billion in 2023 and is likely to reach USD 12.5 billion by 2032. The forecast period from 2024 to 2032 reflects sustained demand from tire manufacturing, automotive production, and industrial rubber applications. The Rubber Processing Chemicals Market is expected to grow at a CAGR of 4.5% during 2024–2032.

The demand case is grounded in product performance. Rubber processing chemicals strengthen rubber and make production smoother and more efficient. Common chemical types include accelerators, anti-degradants, processing aids, and curing agents, each supporting improved manufacturing outcomes and better product performance under demanding environmental conditions.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/rubber-processing-chemicals-market#form

A structured Rubber Processing Chemicals Market forecast points to an industry shaped by practical manufacturing needs. Durable tires, stronger industrial rubber products, and high-performance additives remain central to future demand. The market forecast also shows why chemical suppliers are aligning products with sustainability and performance requirements.

Market Segmentation Analysis

The market is segmented by Product Type into Anti-degradants, Accelerators, Flame Retardants, Processing Aids/Promoters, and Others. Anti-degradants led the market with 50% of the total share in 2023. These chemicals protect rubber from degradation caused by oxygen, ozone, and environmental factors, supporting longer product life.

The market is segmented by Application Type into Tire and Non-Tire. Tire represents the largest application share because tire manufacturing is the biggest consumer of rubber processing chemicals. Demand is reinforced by growing automotive production and increasing emphasis on fuel-efficient and durable tires.

The market is segmented by Region into North America, Europe, Asia-Pacific, and The Rest of the World. These regions represent the market’s core geographic structure. Regional analysis helps clarify where demand is concentrated and how automotive and industrial industries influence the consumption of rubber processing chemicals.

Regional Market Insights

Asia-Pacific leads the global market and is the fastest-growing region. The region’s growth is driven by high automotive production and industrial growth in China, India, and Japan. Large tire manufacturers and rising demand for industrial rubber products further support the region’s market position.

North America is a well-established market. Demand is supported by automotive and industrial industries, especially for durable and environmentally friendly rubber products. This gives North America a stable role in the global industry outlook for sustainable and high-performance rubber processing chemicals.

Emerging Trends Shaping the Rubber Processing Chemicals Market

The market is seeing stronger focus on sustainable rubber processing chemicals. Strategic alliances, including joint ventures, have emerged in recent years. Eastman Chemical Company’s 2023 joint venture with several major tire manufacturers highlights the push to improve environmental performance in tires and rubber products.

Product innovation is also moving toward lower emissions and high-performance protection. Lanxess launched low-VOC additives in 2023, and SI Group introduced Weston 705 in 2022. These developments show how environmental compliance and durability needs are shaping the future competitive landscape.

Key Growth Drivers of the Market

- The tire industry’s large consumption base creates consistent demand for rubber processing chemicals.

- Fuel-efficient and durable tire requirements increase the need for specialized additives with performance benefits.

- Industrial rubber product demand supports chemical use in applications requiring strength and environmental resistance.

- Anti-degradants protect rubber from oxygen, ozone, and environmental degradation, extending product lifespan.

- Sustainability-focused product development supports demand for eco-friendly and low-emission processing chemicals.

Competitive Landscape

Top Companies in the Market

Akzo Nobel N.V.

Arkema

BASF SE

Behn Meyer

Eastman Chemical Company

KUMHO PETROCHEMICAL

Lanxess

Paul & Company

R.T. Vanderbilt Holding Company, Inc.

Solvay

Conclusion and Strategic Outlook

The Rubber Processing Chemicals Market forecast indicates a move from USD 6.0 billion in 2023 to USD 12.5 billion by 2032, supported by a 4.5% CAGR during 2024–2032. Demand is linked to automotive production, tire durability, industrial growth, and sustainability-led innovation. The industry outlook remains steady, with performance chemistry central to future competitiveness.

FAQs – Rubber Processing Chemicals Market

What is the Rubber Processing Chemicals Market forecast?

The Rubber Processing Chemicals Market is forecast to reach USD 12.5 billion by 2032. The market was valued at USD 6.0 billion in 2023.

What CAGR is expected through 2032?

The Rubber Processing Chemicals Market is expected to grow at a CAGR of 4.5% during 2024–2032. This reflects steady demand from tire and industrial rubber applications.

What are the main market drivers?

The main drivers include automotive production, tire manufacturing, industrial rubber demand, and durability requirements. Sustainability-focused chemical development is also influencing market direction.

Which region leads the market?

Asia-Pacific leads the Rubber Processing Chemicals Market and is also the fastest-growing region. China, India, and Japan are important demand centers due to automotive and industrial activity.

What is the strategic investment outlook?

The strategic outlook is stable because rubber processing chemicals are linked to essential performance requirements. Companies focused on durability, sustainability, and application-specific performance may be better positioned.